One of the earliest large-scale battery storage projects in the United States came online in 2003 in Fairbanks, Alaska — the 'Gateway to the Arctic' — where extreme cold and generator failures could quickly trigger blackouts on the city's isolated grid. At 40 MW, it was the largest battery system in the world at the time, providing spinning reserve via nickel-cadmium cells designed for cold weather. Today, the world’s largest energy storage project is part of a solar-plus-storage system in California, which came online in 2024 with 3 GWh of BESS capacity.

In the intervening years, battery storage has evolved from a niche reliability tool into a market-participating grid asset. Systems now earn revenue across energy arbitrage, ancillary services, capacity markets, and demand response. In 2026, the sector is expected to attract $25.2 billion in capital investment, and the projects seeking that capital are orders of magnitude more complex than their predecessors.

.jpeg)

Investors underwriting these projects must understand technical performance, contractual structure and limitations, and market operations. Even at advanced stages of development, uncertainties remain across each dimension, and in late-stage transactions the assumptions behind them often determine project outcomes.

This piece examines the diligence blind spots within those assumptions that most consistently shape investment outcomes in late-stage utility-scale BESS.

What makes BESS diligence different

Battery storage doesn't fit cleanly into the diligence frameworks developed for solar or wind. The revenue stack is more complex, the degradation dynamics are more operationally sensitive, and the technology introduces insurance and compliance exposures that don't have clean analogs in other asset classes.

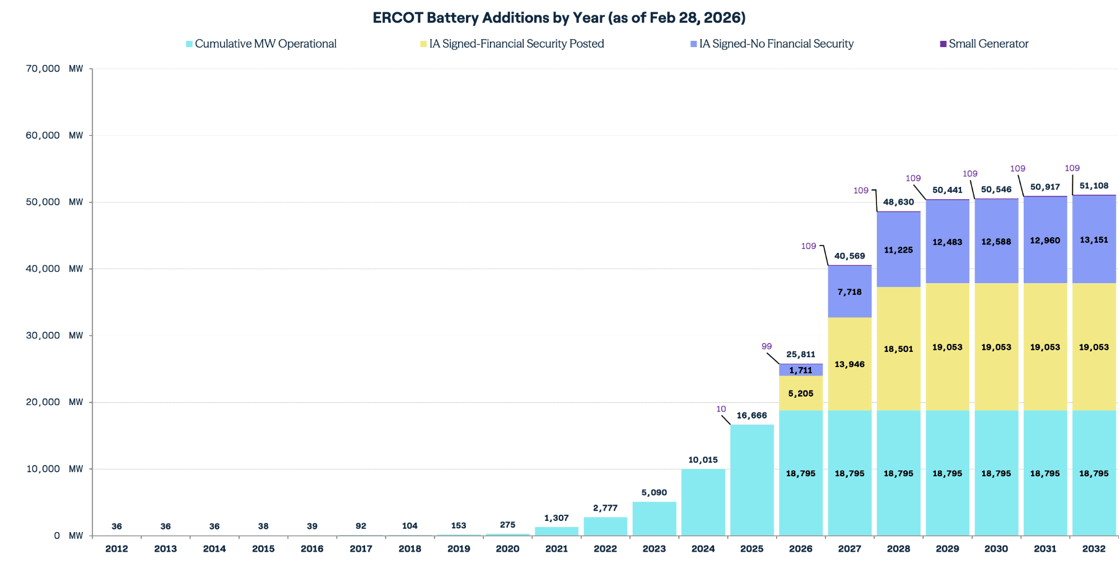

Across the United States, 980 GW of battery storage is seeking interconnection. CAISO and ERCOT dominate the development pipeline, with around 177 GW and 175 GW of storage capacity in their queues, respectively. Together they account for about half of all proposed storage nationwide. The two markets expose investors to fundamentally different risk profiles.

In ERCOT’s energy-only market, storage revenues are driven primarily by merchant arbitrage and ancillary services. Asset performance varies widely and depends heavily on siting, congestion dynamics, nodal pricing elasticity, and dispatch strategy. Diligence therefore requires forward-looking nodal modeling to stress-test saturation risk, cannibalization, and scarcity pricing assumptions. Revenue models must also account for RTC+B, implemented in late 2025, which integrates batteries into real-time co-optimized dispatch which may reshape ancillary market saturation and arbitrage spreads.

In CAISO, storage revenues are often anchored by Resource Adequacy (RA) capacity payments supplemented by arbitrage, creating a more structured revenue stack than merchant markets. Diligence therefore focuses less on nodal price volatility and more on capacity accreditation and regulatory durability. Under the CPUC’s Slice-of-Day (SOD) framework, load-serving entities must demonstrate sufficient capacity for each hour of the day rather than a single monthly peak. Storage resources must therefore validate four-hour discharge capability, charging sufficiency, and compliance with evolving CPUC and CAISO standards. Underwriting must also consider how rule changes could affect capacity counting and long-term RA revenue stability.

These structural differences determine where diligence effort should concentrate. In the following sections, we examine the three areas where late-stage BESS transactions most commonly reprice or fail to close.

"In this environment, success hinges on the discipline to say 'no' early. Effective due diligence means identifying risks early, even for late stage entries. Decisions must be made soon enough to re-trade the price, like uncovering a $5 million grid upgrade late in the game, or having the conviction to kill a bad deal before you’ve sunk significant pursuit capital into it.” — Cyrus Etemadi, Program Director, Grid-Scale, BESS Development

Cost (un)certainty

BESS projects are highly capital intensive, with most lifecycle costs incurred before commercial operation. That arithmetic makes cost certainty a disproportionate driver of equity returns, and it makes the gap between a developer's cost representation and actual project costs one of the most consequential diligence questions.

Interconnection upgrade obligations are a primary source of cost uncertainty. Recent research finds network upgrades averaged about 70% of total interconnection costs for projects withdrawn from U.S. interconnection queues between 2019-2023. Because upgrade costs can dominate total interconnection spending, even modest changes to upgrade scope can materially affect project economics.

Interconnection studies are based on a project’s proposed capacity and operating profile. For co-located projects, changes to storage configuration or operating assumptions may trigger a material modification review. For standalone assets, charging strategies, Short Circuit Ratio (SCR) conditions, and evolving grid constraints can also alter upgrade requirements as studies progress. These changes can introduce multimillion-dollar network upgrades and force transaction re-pricing. Investors can mitigate this risk by validating study assumptions, confirming upgrade cost allocation across projects, and ensuring upgrade scope is locked through executed interconnection agreements prior to notice to proceed.

Procurement conditions introduce another dimension of CapEx risk. Battery modules and power electronics represent a large share of total project cost, and pricing is sensitive to global supply chain conditions and raw material costs, particularly lithium and critical minerals. The current tariff environment compounds this exposure: sourcing from sanctioned suppliers can forfeit ITC eligibility entirely, while compliant alternatives often carry higher equipment costs. The compliance framework governing these thresholds is still evolving, and procurement assumptions made at project inception may not hold at financial close.

.jpeg)

As a result, late-stage diligence should focus on CapEx certainty and schedule protection, validating interconnection upgrade obligations, quantifying cost impacts of permit requirements, reconciling EPC scope across contractors, and confirming supply chain compliance before notice to proceed.

Revenue defensibility

In merchant markets such as ERCOT, battery revenues depend heavily on dispatch strategy across arbitrage and ancillary services. As storage penetration rises, ancillary service margins compress and projects increasingly rely on energy arbitrage, which requires more frequent cycling.

A common diligence blind spot arises when revenue models assume more cycling than the battery can sustain without accelerating degradation. If realized dispatch exceeds modeled assumptions, degradation can accelerate and reduce usable capacity over time.

Lithium-ion systems typically experience low single-digit annual capacity degradation under moderate cycling, but higher dispatch frequency can increase this by 100 to 200 basis points, meaningfully reducing capacity over time.

Diligence should test whether modeled revenues are physically achievable given the system's operating constraints. That means verifying dispatch assumptions against:

- Degradation curves and warranty thresholds

- Auxiliary load and real round-trip efficiency, including parasitic HVAC losses

- Charging constraints that may limit grid-charging windows

- Planned augmentation timing and capital reserves

If revenue models require sustained over-cycling, projects may experience accelerated degradation, reduced later-year revenues, and lower residual asset value.

Risk transfer and bankability

By the time a project reaches the pre-NTP or procurement stage, financial models are typically fully stress-tested and commercial terms appear settled. At this point, bankability depends less on modeled returns and more on whether technical, regulatory, and construction risks have been transferred through enforceable contracts. Projects that appear viable on paper can still struggle to close if lenders, insurers, or tax equity investors identify unresolved exposure during diligence.

Diligence therefore focuses on confirming that risk has been transferred through EPC guarantees, O&M obligations, insurance coverage, and supply-chain compliance provisions, and that all financing conditions have been satisfied. Insurance is particularly important for utility-scale BESS. Industry broker estimates place annual premiums at roughly 0.3 to 1.2 percent of total system value, with pricing influenced by battery chemistry, system design, and fire protection features; projects with adverse risk profiles — such as NMC chemistry, limited fire suppression, or exposure-prone locations — may attract rates toward the higher end of this range.

Common diligence gaps emerge around NFPA 855 compliance, fire suppression systems, thermal monitoring, and site layout. For example, a developer may specify container spacing of three feet between battery enclosures to maximize site density. During underwriting, insurers may require spacing consistent with applicable fire codes, including NFPA 855, and may impose distances beyond the code minimum to reduce fire propagation risk. If identified late, these issues can require design revisions, increase insurance premiums, or delay financial close.

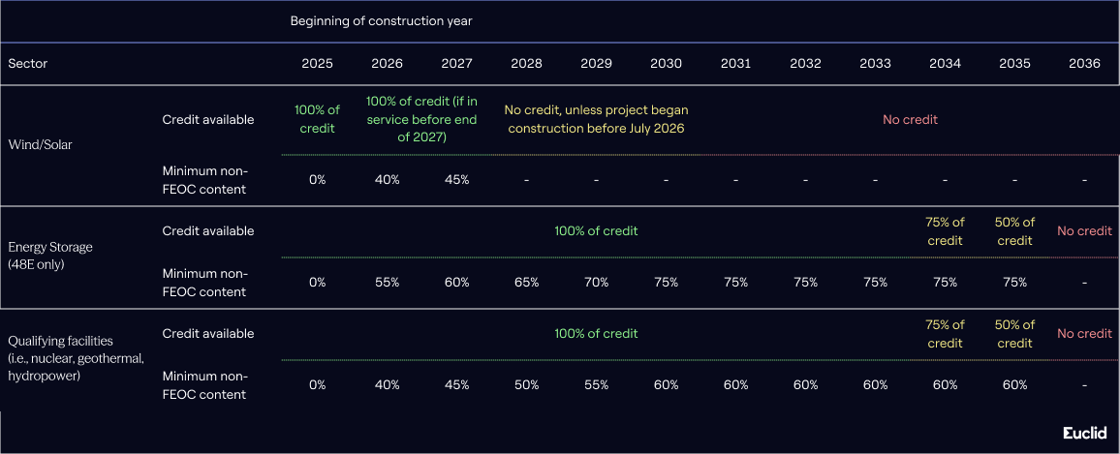

Supply-chain compliance presents another risk. Restrictions related to foreign entities of concern (FEOC) and domestic content thresholds can affect investment tax credit eligibility and the amount of tax equity proceeds available at closing. Last year, the OBBBA introduced a MACR-based compliance framework and a “Reason to Know” standard that goes beyond vendor certifications. For a deeper explanation of how the MACR framework works in practice, see our analysis of Notice 2026-15.

For investors, the objective of late-stage diligence is straightforward: confirm that technical, regulatory, and supply-chain risks have been contractually transferred and that financing conditions are fully satisfied before construction begins.

Up next

For investors entering projects near construction, diligence is less about validating project economics and more about stress-testing the assumptions that underpin them. That distinction matters more as the market scales: utility-scale storage alone is expected to reach 20 GW and 62 GWh of new deployments in 2026. At that volume, the ability to identify hidden risks early is a genuine competitive advantage.

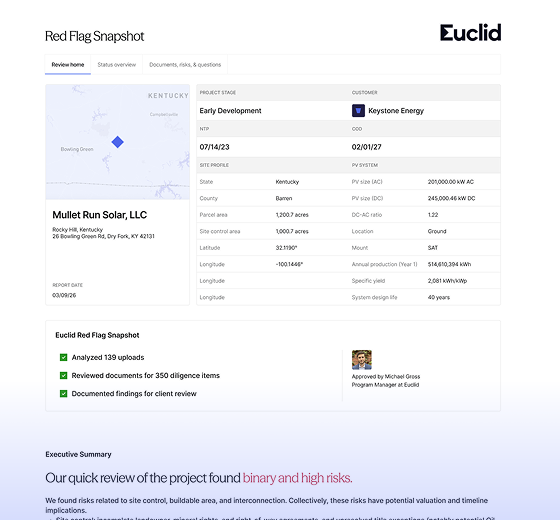

Announcing Red Flag Snapshot

We built Red Flag Snapshot because portfolios land on desks with days — sometimes hours — to decide whether to bid, and the old way of figuring out if a project is worth pursuing just can't keep up.

Here's how it works: send us a data room, and we'll deliver a structured risk screening by the next business day. Binary risks, document gaps, and prioritized open questions — all prepared by Euclid's renewable energy experts using a framework refined across more than 1,000 solar and storage projects.

The result is a clear early signal on whether a project deserves deeper diligence, fast enough to matter in competitive transactions.

Talk to us about running a Red Flag Snapshot on your next opportunity.

Enjoying this deep dive?

Stay up to date on market insights for teams who build, buy, and finance renewable projects.