A closer look at Notice 2026-15

The passage of the OBBBA last July marked the most abrupt shift in clean energy policy in decades. The law significantly altered project economics by rolling back key provisions of the 2023 Inflation Reduction Act. As a result, only three federal tax credits remain available: §45X (Advanced Manufacturing Production Credit), §45Y (Clean Electricity Production Credit), and §48E (Clean Electricity Investment Credit). Each is now subject to stricter domestic content and supply chain requirements.

After months of anticipation, the U.S. Treasury and IRS released Notice 2026-15 earlier this month, providing interim guidance on how to apply safe harbors when determining whether a taxpayer satisfies the Material Assistance Cost Ratio (MACR) requirements related to Prohibited Foreign Entities (PFEs) for tax credit eligibility. The guidance imposes stricter standards on foreign ownership and sourcing than those established under the Inflation Reduction Act.

In this special edition of our newsletter, we examine how to calculate the MACR, outline the specific safe harbors for material assistance, explain the rules governing PFE ownership structures, and assess what these changes mean for capital providers and developers.

What’s In The Guidance

- The Material Assistance Cost Ratio (MACR): Notice 2026-15 provides the mechanism for calculating the MACR, which is a percentage of total direct costs attributable to non-prohibited foreign entities. If MACR falls below the statutory threshold, the tax credit is denied.

- Safe Harbors: Notice 2026-15 provides a series of safe harbors to reduce the compliance burden on taxpayers by including De Minimis Exceptions of upstream supply-chain tracing, reducing the modelling burden through cost allocation, and allowing supplier certifications as proof.

- PFE Definitions: While Notice 2026-15 focuses primarily on material assistance calculations, it reiterates the statutory framework for determining when an entity is treated as a prohibited foreign entity, such as ownership thresholds, ownership tracing, and the “effective control” test. Importantly, even with 0% PFE, an entity may still be treated as a PFE if it relies on contractual rights, such as technology licensing or intellectual property agreements, which would grant a foreign entity “effective control.”

Determining Material Assistance

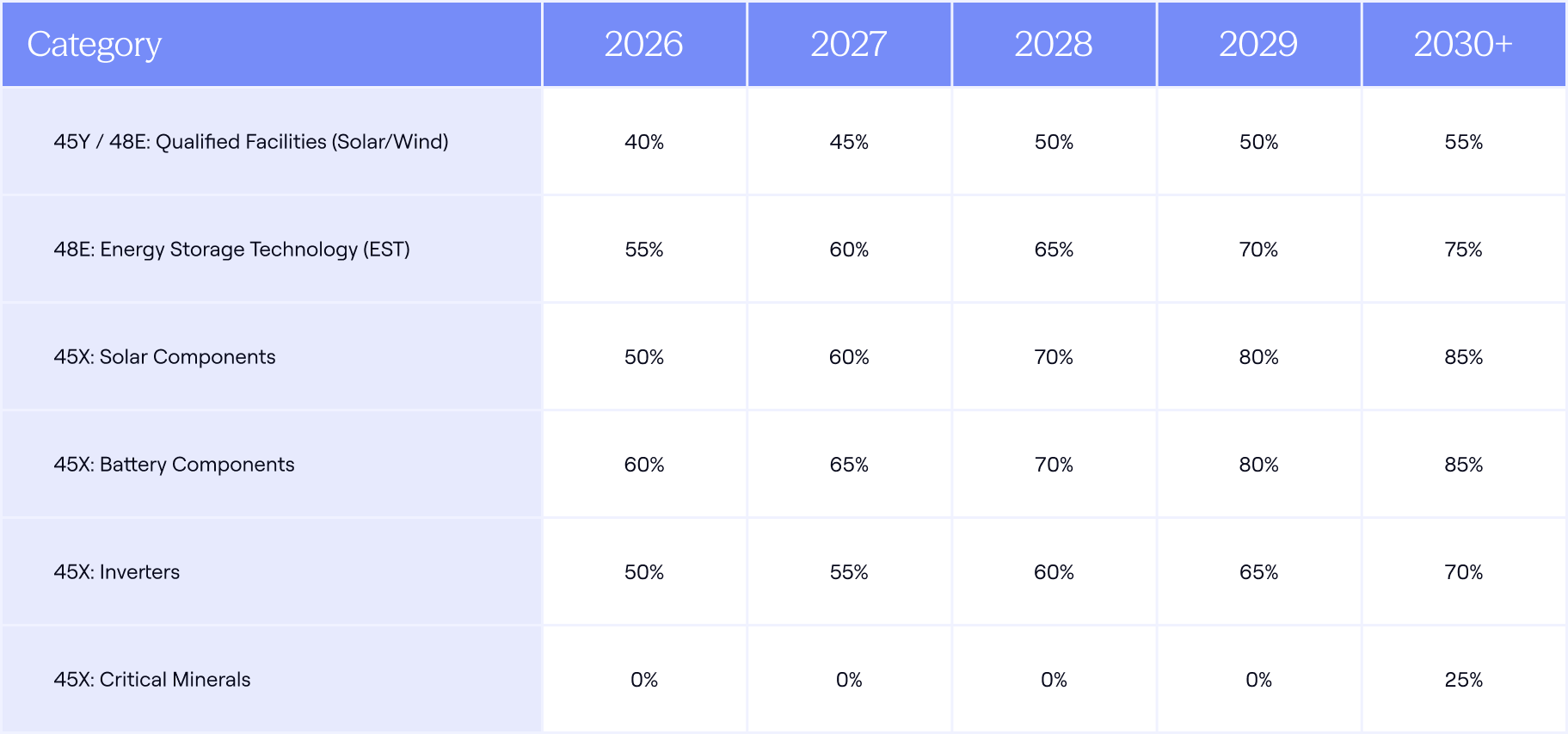

Notice 2026-15 clarifies that compliance with the Material Assistance Rules hinges on calculating the MACR for each qualified facility, component, or energy storage technology. The MACR measures the percentage of total direct costs attributable to non-PFEs. If that percentage falls below the statutory threshold, the facility is ineligible for the credit.

Thresholds vary by technology and increase over time, effectively tightening sourcing requirements in future years. Technologies with more concentrated foreign supply chains, such as wind components and battery materials, are more sensitive to upstream PFE exposure and have higher initial MACR allowances to reflect current supply chain realities. Certain critical minerals are also subject to separate statutory treatment, which the Treasury plans to release guidance on in 2027.

In practical terms, MACR turns supply-chain exposure to PFEs into a credit eligibility test across various aspects of the project life cycle:

- Facility-level testing: The MACR test is applied separately to each facility (solar inverter block, wind turbine, or standalone BESS enclosure). A single non-compliant unit won’t exempt an entire portfolio, but that specific facility would lose credit eligibility.

- Interconnection property: Qualified interconnection property requires its own MACR calculation. If interconnection fails, credits on that spend are lost, and if the facility fails, the entire credit, including interconnection, is disallowed.

- 80/20 rule: For projects qualifying under the 80/20 rule (facilities where the ‘Fair Market Value’ of used equipment is 20% of the total value), only new components are included in the MACR calculation. This generally reduces FEOC exposure compared to greenfield builds.

- De minimis and averaging relief: Components costing less than 10% of the project total cost may be flexibly assigned across the same-year facilities, and small storage systems (<1 MW) may use cost averaging. These provisions ease the tracking burdens of small-scale projects but don’t eliminate exposure to major cost drivers, such as battery cells and modules.

Example: Battery Storage MACR Calculation

Consider a developer planning to build a 100 MW storage project with $100 million in direct costs. The battery modules — classified as one of the project’s manufactured products — represent $50 million of that total. If 60% of those modules are sourced from a Prohibited Foreign Entity (PFE), the MACR calculation would be as follows:

- PFE Costs: 60% of $50M = $30M

- Calculation: ($100M Total - $30M PFE) / $100M Total = 70% MACR

- The Result: Since the 2026 threshold for energy storage is 55%, this project would pass and is eligible for the full tax credit.

However, beginning in 2030, the same project would fail the MACR test. At that point, the required threshold for the §48E energy storage technology credit increases to 75%, rendering the developer ineligible for the tax credit under the same sourcing assumptions.

Safe Harbors

Safe harbors are critical to making the MACR workable. They define the "Scope of Determination," minimizing the due diligence burden by limiting the depth to which companies need to follow components, subcomponents, or raw materials upstream in the supply chain.

To limit the depth of upstream tracing, Notice 2026-15 defines which components must be evaluated, using the domestic content tables from previous guidance provided from 2023-25. The Treasury is required under the notice to release updated tables by the end of this year.

Table Example: A developer of a battery energy storage system (BESS) uses the table below from Notice 2025-08 to identify which battery components must be included in their MACR.

It also creates a "stop-loss" on tracing. For example, if the Table defines a "Battery Module" as the relevant component, the developer calculates MACR based on the Module's origin, without needing to trace the individual cells or separator films inside it (until updated tables are released later this year).

In addition, the Notice permits reliance on supplier certifications regarding PFE status, provided the taxpayer “does not know or have reason to know that any of the certifications are inaccurate.” This is not a "blind eye" provision. If public filings or reputable trade reports indicate a supplier has PFE ties, a certification to the contrary will not protect the taxpayer. Certifications must meet specific content requirements and be retained for six years (in alignment with the tax credit recapture period).

PFE Definitions

The Notice provides taxpayers with guidance on defining PFE ownership. It provides a 25% individual ownership threshold or a 40% aggregate ownership threshold by PFE interest.

Notice 2026-15 also targets licensing agreements that grant "effective control" over the facility. This includes rights to shut down the plant, access proprietary data, or restrict who the facility can sell to. A standard "right to use" license is usually safe; a "right to control" license is the deal breaker.

Intellectual property or licensing agreements that go beyond standard commercial terms could also constitute "effective control." If a license grants a PFE the right to determine production quantities, restrict sales territories, or access non-public operational data, the licensee is treated as a PFE. A standard technology license (paying royalties to use LFP chemistry) remains permissible. However, a license that allows the foreign licensor to remotely shut down the battery system or dictate maintenance schedules crosses the line into "effective control.”

This still leaves some ambiguity, which the Treasury has acknowledged and said it will address in future supplemental guidance.

Key takeaways for capital providers and developers

While comprehensive regulations are still forthcoming, the interim framework suggests a more flexible, cost-weighted compliance model than the no-Chinese-products approach some had anticipated.

Under the IRA, projects could qualify for a 10% bonus credit if they met domestic content thresholds. Under the OBBBA framework, a project either satisfies the applicable threshold and receives the credit, or fails and receives nothing. As a result, developers and investors must exercise far greater diligence to ensure compliance with the safe harbor requirements.

Timing will also be critical. A project’s beginning-of-construction date determines which year’s MACR threshold applies, and those thresholds decline annually. Market participants are effectively racing against a moving target. If allowable PFE content drops from 45% to 20% on January 1, 2029, developers will face strong incentives to place projects in service by December 31, 2028 — creating a potential “cliff-edge” bottleneck for interconnection and construction capacity.

Reliance on simple vendor affidavits may not be sufficient. To withstand an IRS audit under the new “Reason to Know” standard, developers will likely need structured supply-chain mapping and robust documentation. “Audit defense files,” including independent verification and digital traceability records, may soon become standard conditions precedent to financial close.

The Euclid Perspective

“Supply chain diligence is no longer just a compliance exercise, it is now one of the most important underwriting metrics for bringing BESS projects to NTP. Notice 2026-15 transforms MACR into a manageable, modelable standard that can allow capital to flow again.” — Cyrus Etemadi, Program Director, Gridscale BESS Development

“This guidance reduces uncertainty in the near-term, but the industry needs to be ready for more intense scrutiny in future requirements. Tax credits are only as strong as the audit-ready compliance behind them. Robust supply-chain diligence, supplier certifications, and MACR modeling are critical to protecting tax credit value.” — Ryan Guay, Co-founder

What Comes Next?

Notice 2026-15 provides the first real operating framework for applying the FEOC rules, but this is far from the last. The Treasury has indicated that more comprehensive proposed regulations are coming, particularly around the definition of PFE and the unresolved effective control standards. This remains the area of greatest legal ambiguity and potential transaction risk.

Notably, Treasury’s framing of December 31, 2025 as a beginning-of-construction date for anti-circumvention purposes signals heightened scrutiny of projects claiming a 2025 start date. Additional substantiation requirements could materially affect safe harbor expenditure strategies and late-stage pipeline transactions.

The Notice also directs Treasury to publish updated Domestic Content Safe Harbor tables by December 31. In the interim, taxpayers may continue to rely on the 2023–2025 tables.

The final guidance will be released after a public comment period for this initial guidance, which closes on March 20th, 2026. You can provide your own comment here.

Enjoying this deep dive?

Stay up to date on market insights for teams who build, buy, and finance renewable projects.