Over the last 10 years, the Southwest Power Pool (SPP) showed the rest of the country how quickly renewables can transform a power market. In 2015, wind accounted for 14% of the region’s capacity. By 2025, that had shot up to almost 37%. Abundant wind resources, low-cost land, and expansive transmission infrastructure helped make SPP one of the country’s biggest renewable generation hubs, with some of the lowest wholesale power prices.

Now this success is creating a new set of market dynamics. As deployment of solar and storage accelerate across the region, the market is seeing more congestion, curtailment, negative pricing events, and operational volatility.

At the same time, SPP’s proposed Markets+ initiative aims to increase regional coordination across the Western Interconnection, an effort that could reshape how renewable power is dispatched, traded, and monetized across a much larger geographic footprint.

Though solar only accounted for 0.7% of SPP’s total energy production last year, the region’s biggest concern isn’t adding more renewable generation. The main challenges it’s facing now are managing flexibility, transmission, and coordination in a grid that’s saturated with low-cost renewable power.

Renewable saturation is reshaping SPP market economics

SPP’s renewable buildout was initially driven by wind. But solar and storage are becoming bigger components of the development pipeline, adding new generation patterns to a grid that’s already highly shaped by variability. By 2050, 42–130 GW of solar additions are expected, along with 22–59 GW of battery storage. New wind, in comparison, is forecast to be 20–48 GW.

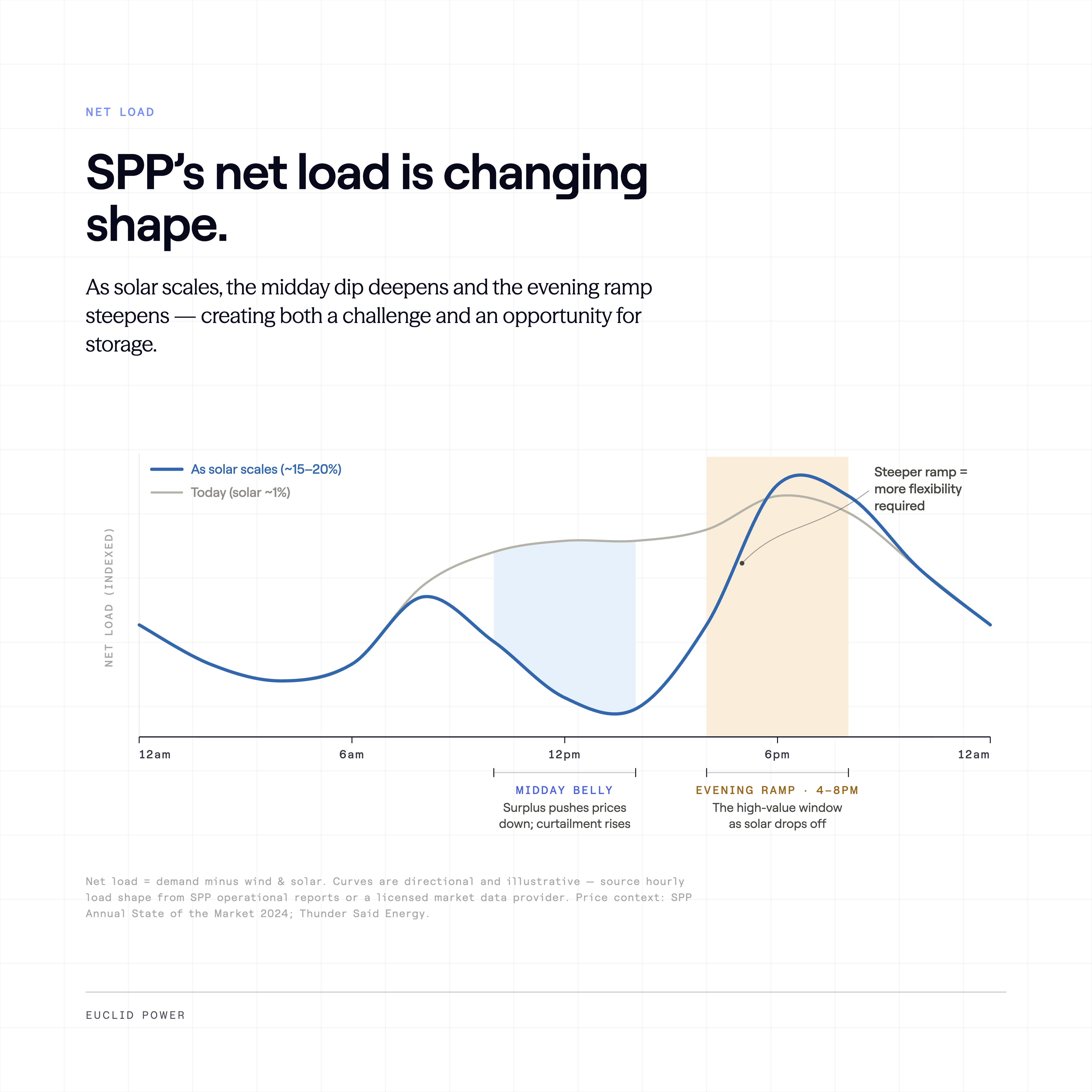

This transition is changing market economics in key ways. First, rising renewable generation is causing power prices to fluctuate more throughout the day. Solar deployment is pushing daytime prices down, while strong wind generation leads to oversupply during low-demand hours. This has led to more negative pricing events, particularly during periods of high renewable output combined with transmission congestion. SPP has even developed its own version of CAISO’s duck curve, which shows a midday dip in the net load curve followed by a rise in the evenings when solar generation drops off.

Historically, renewable project economics in SPP were mostly driven by resource quality. Transmission and congestion exposure have always been critical in the region due to the large geographic distance between wind-heavy Western zones and major load centers like Dallas-Fort Worth and Oklahoma City. Now locational factors are becoming even more acute, and projects need to be able to effectively navigate operational constraints. Developers are paying closer attention to congestion, curtailment (when renewable output is purposely reduced because the grid can’t absorb it all), transmission access, and local price volatility.

This is especially important because SPP’s transmission system, while extensive, is straining under the pace of renewable deployment. Congested transmission is creating bigger gaps between local project prices and broader regional power prices, which makes future project revenues less predictable for developers.

The market is also getting more operationally complex. Average power prices aren’t reliable indicators of project value anymore; developers have to account for a wider range of market and transmission risks to get an idea of how projects will perform.

Storage and flexibility are becoming more valuable

Given how saturated SPP is with renewable generation, its next wave of value creation likely won’t come from adding more renewables; it will be based on building in more grid flexibility to leverage existing assets—in other words, adding battery storage.

Since batteries can charge when electricity prices are low and discharge when they’re high, operators can use them to take advantage of larger price spreads. Storage can also generate revenue through ancillary services, which are a core component of the BESS value stack in SPP. For example, SPP offers Regulation (short bursts of power to correct frequency deviations), Spinning Reserve (standby capacity that can replace drops in generation or spikes in demand), and Supplemental Reserve (dedicated grid capacity that can discharge quickly to cover sudden supply shortfalls or grid contingencies).

.png)

As solar capacity grows from <1% to a projected 10–20%+ of SPP’s generation mix over the next decade, intra-day price spreads will continue to widen, improving BESS energy arbitrage economics structurally, not cyclically. SPP’s growing frequency of negative-price hours also means well-positioned BESS can charge at effectively zero or negative cost, dramatically improving round-trip efficiency economics and boosting project IRRs. Finally, the 4PM-8PM window in SPP is becoming a high-value dispatch zone as solar drops off and wind variability creates supply uncertainty. BESS positioned to capture this window commands a growing revenue premium.

SPP is seeing some of the same dynamics that helped drive storage growth in ERCOT—namely price volatility and negative pricing events. However, adding more battery storage won’t address all the challenges created by renewable saturation. Projects still face high market uncertainty, with project value depending more on how effectively operators can forecast prices, optimize dispatch, and respond to market conditions in real time.

The rise of hybrid projects reflects this shift, too. Co-located solar and storage can improve value capture by reducing curtailment exposure and letting developers optimize when energy is delivered into the market.

Markets+: A broader shift in western market design

At the same time that SPP’s internal market dynamics are evolving, it’s aiming to expand its role across the Western Interconnection through Markets+, a day-ahead and real-time market for western utilities and balancing authorities. With independent governance, Markets+ is essentially a new market built on existing operator infrastructure, specifically the Western Energy Imbalance Service (WEIS). Markets+ aims to improve regional coordination, dispatch efficiency, renewable integration, and transmission utilization across a larger geographic footprint.

One big change is the introduction of a centralized day-ahead market, which lets participants buy and sell electricity a day before it’s actually needed. Instead of each utility forecasting its own demand and arranging power purchases, the market can optimize dispatch across a larger region, helping move lower-cost electricity to where it’s needed most and making it easier to integrate renewable energy.

The proposal reflects a broader industry trend: as more renewables are deployed, it’s more valuable to coordinate across a wider market. Balancing supply across a larger area can help smooth renewable variability by letting areas with excess generation export power to areas with tighter supply conditions. It also helps the market make better use of the available transmission capacity and cut down on the need to use natural gas plants.

Markets+ also represents a different philosophy around how western power markets should evolve. Many western utilities want the efficiency benefits associated with organized markets, but don’t want to give up their operational autonomy to a centralized transmission organization. Markets+ addresses this concern by offering a more flexible governance structure than traditional RTO models.

This puts Markets+ in direct competition with CAISO’s Extended Day-Ahead Market (EDAM), another major effort to expand organized market coordination across the West. While both initiatives aim to improve renewable integration and regional efficiency, they have different governance structures, operational controls, and market philosophies.

With increased renewable penetration, market coordination itself is becoming a form of infrastructure, and for developers this evolving market structure adds commercial and operational complexity. Changes in dispatch rules, congestion patterns, transmission utilization, and pricing dynamics can materially affect project economics over time.

Transmission and interconnection: SPP’s primary constraints

Transmission is the biggest constraint shaping SPP’s next development phase. SPP’s transmission network has historically been one of the region’s major competitive advantages, helping enable large-scale renewable deployment across geographically diverse areas. But in many parts of the system, transmission capacity can’t keep up with the pace of new generation development.

Interconnection queues are heavily backlogged; SPP has about 150 GW in its generation interconnection queue, including 22 GW of battery storage and 21 GW of solar. SPP has adopted FERC Order 2023, which includes cluster study reforms designed to clear the backlogged interconnection queue and introduce more certainty around upgrade costs. Developers who understand the new rules and can navigate the transition period will have a structural timing advantage.

As a result, the gap between queued projects and financeable projects is widening. Like in other renewable-heavy power markets, the challenge is the ability to move energy to where and when it’s needed without overwhelming grid infrastructure.

From scale to coordination

SPP offers an early look at the future of renewable power markets. For years, the industry’s focus was adding renewable capacity as quickly as possible. Today, the challenge is different: orchestrating a grid filled with low-cost, variable generation.

Several SPP-adjacent states (Colorado, New Mexico, and indirectly Texas) have adopted aggressive clean energy targets that are driving utility procurement of new solar and battery storage capacity, creating additional PPA demand beyond purely merchant projects. In addition, Oklahoma, Kansas, and the broader SPP footprint are attracting significant hyperscaler data center investment, driven by land availability, grid access, and state incentives. This new load is creating demand for long-term clean power PPAs—the type of bankable offtake that enables project financing.

Markets+, storage growth, and transmission constraints all point toward the same conclusion: in the next phase of the energy transition, flexibility and operational intelligence will become just as valuable as generation itself.

Enjoying this deep dive?

Stay up to date on market insights for teams who build, buy, and finance renewable projects.