Every power plant begins its life with an investment thesis. During development or acquisition, teams model production under representative site conditions, validate costs, anticipate the shape of O&M, and calculate future revenue based on their thesis on market conditions. These projections justify project investment, set the capital stack, define investor expectations, and set the baseline against which performance will be judged once a project is operational.

But once a plant transitions into operations, it no longer behaves like a static financial model. It starts behaving like what it truly is: an ecosystem shaped by dynamic environmental forces, aging components, and thousands of small operational decisions.

Ecosystems are not static. Annual weather rarely matches modeled P50 expectations. Components degrade faster—or differently—than assumed. Small problems compound. Increasingly, fleet-level data shows this divergence is not edge-case behavior but the norm: solar projects around the country are underperforming their original P50 energy forecasts, with average shortfalls in the 7–10% range. That gap is not driven by one big failure. It’s driven by many small ones.

In this first installment, we’re going to focus on three places where we consistently see modeled performance diverge from operational reality: soiling, spares management, and downtime assumptions.

Soiling: The model vs field reality

In most models, soiling shows up as a simple haircut: a flat 1–3% annual loss, spread evenly across the year. The assumption underneath that number is usually implicit: rain will take care of the rest, and whatever dust does accumulate will be minor and self-correcting.

In the field, soiling rarely behaves that politely. It is not steady-state. It is lumpy, seasonal, and asymmetric. When dry stretches extend—particularly through summer months—“natural cleaning” stops being a dependable mechanism. Dust builds faster than it comes off, and losses climb nonlinearly.

Field studies across the U.S. increasingly show annual soiling-related energy losses in the 5–7% range, with materially higher losses in semi-arid climates and regions with frequent dust deposits. Losses can vary widely across distances as short as a few miles based on localized pollution, land use, mounting configuration, and proximity to high-traffic areas. Wildfire seasons are intensifying, and even fires hundreds of miles away can cause solar assets to lose up to 6% in annual revenue. For nearby projects, generation losses from smoke can reach into double-digits.

Add a humid morning or dew after a dry spell and the problem can literally harden: dust particlesbind to the glass and turn what should be a simple issue for the rain to wash away into a more expensive routine.

The problem is not that soiling exists (we all know that). The problem is that it often lives in the gray zone: big enough to matter, quiet enough to avoid alarms.

Most portfolios do not “detect a soiling event.” They drift into persistent underproduction versus expectation. By the time the issue is obvious enough to trigger action, the lost energy is already gone. Worse still, many developers and IPPs do not explicitly model module washing costs at all, or define a wash strategy before acquiring or building a project—leading to decades of unexpected additional costs.

Small faults: When “quick resets” turn into chronic drag

Downtime is often modeled as a rounding error—0.5% annually, sometimes less, sometimes nothing at all. A string trips. An inverter faults. Someone resets it. The plant is back online. In spreadsheets, the assumption is simple: small problems are fast problems.

That assumption is wrong. In the field, small problems are often the beginning of a much bigger story. Euclid Senior Project Manager Killian McDonald puts it this way:

“One-off events are not always—but can often be—symptomatic of larger systemic issues. If a fault in a DC combiner box takes out a large section of an inverter’s input, replacing the fuse may restore production. But if the fault was introduced because every combiner was entered from the top instead of the bottom, water intrusion will reintroduce the same failure during every rain event until the root cause is addressed.”

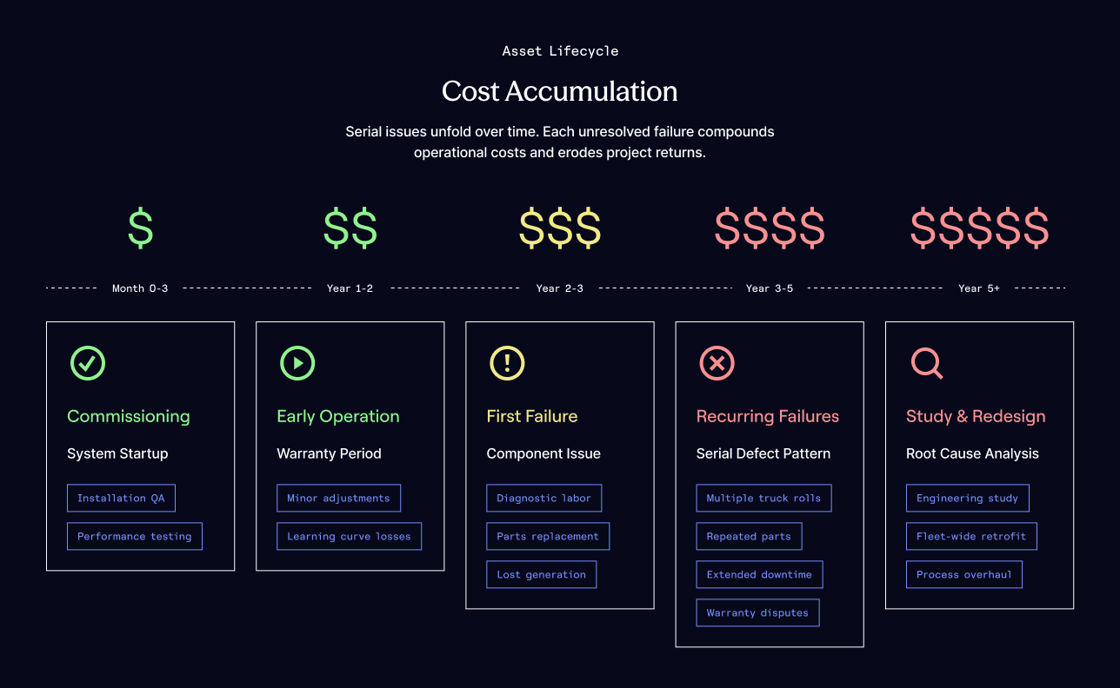

This kind of downtime is financially corrosive because it hides repeat, condition-driven faults and multi-visit repairs. A plant can remain technically “available” while quietly underproducing for months.

Fleet-scale data makes this distinction visible. Across the U.S. solar fleet, operating projects underperform their original P50 energy forecasts by an average of 8.6% even while headline availability metrics remain strong. The gap is not driven by catastrophic outages; it is driven by partial outages, slow-to-repair faults, and degraded operation that never quite trips an alarm. Inverters account for more than one-third of total energy loss events, many of which leave systems technically “available” but operating below capacity for weeks or months. The result is not a plant that is down, but a fleet that is chronically underproducing.

This is why “downtime” is often a misnomer. In real operations, availability is constrained by repair timelines measured in days to months, not minutes. Energy loss rarely arrives as a single, auditable event. It arrives as nuisance alarms that fade into background noise, repeat truck rolls that never quite fix the issue, and partially degraded operation that quietly compounds quarter after quarter.

Spares: The cheapest parts cause the longest losses

Spares rarely show up in an investment thesis in any meaningful way. If they appear at all, they are usually treated as a working-capital detail: replacement parts will be available when needed, warranties will cover major failures, and anything truly serious will be handled as a one-off event.

In practice, neglecting a spares strategy is one of the most avoidable drivers of prolonged underperformance. Across the U.S. fleet, inverter and DC-side component failures account for a disproportionate share of lost energy. Industry inspections show that inverters alone drive more than one-third of total PV power loss events, while DC-side issues (combiner box and string faults) continue to grow as a share of lost production year over year.

None of these failures are exotic. Nearly all are fixable. The constraint is not diagnosis; it is time to repair. That time-to-repair is where spares quietly become a production variable.

Many portfolios carry little to no on-site inventory beyond a handful of fuses. When a combiner board, inverter fan assembly, or communication card fails, the clock starts ticking—not on the failure itself, but on procurement. Lead times stretch from days to weeks to months, especially for older inverter models, discontinued SKUs, or equipment with evolving bills of materials. In those cases, availability on paper remains high, but effective capacity stays depressed while the system waits for parts.

This is the spares paradox: the parts that matter most to uptime are often the cheapest, least visible, and least planned for. And because their absence rarely triggers alarms, the loss they introduce is easy to normalize and hard to recover.

Tending your garden: how the best operators optimize their asset performance

There are steps project owners can take to materially improve outcomes, but they will require a shift in mindset. Optimizing performance is not about eliminating every fault; it’s about reducing unforced errors and shortening the half-life of loss.

Euclid Co-Founder Brian DeMaio puts it plainly:

“Some people underestimate what it takes to operate a fleet. Building a great asset management team means hiring people who can read a spreadsheet and read the field. If your asset manager has never stepped foot in the field and can’t diagnose technical issues, you’re not managing assets—you’re just reporting on losses.”

The right asset management team is the foundation. But structure alone is not enough. On the challenges we’ve covered here, the best operators behave differently.

- Soiling. The best operators treat soiling as a controllable economic variable, not an O&M checkbox. They model it as seasonal and site-specific, not flat and annual. They monitor production deltas closely enough to identify creeping loss before it becomes a quarterly drag. And they set wash cadence based on marginal revenue recovery, not the calendar.

- Small-faults and downtime. The best operators do not just log failures; they track patterns. Repeat interventions are treated as leading indicators. Nuisance alarms are treated as early warnings. Time spent diagnosing root causes is budgeted as a real production variable, especially as fleets age and “reset and return” stops being a reliable operating strategy.

- Spares. The best operators identify the components that most often extend outage duration and plan inventory accordingly. They treat long lead-time parts as operational risk, not procurement trivia. And they accept that capital tied up in the right spares is often the cheapest way to buy back lost energy.

Enjoying this deep dive?

Stay up to date on market insights for teams who build, buy, and finance renewable projects.