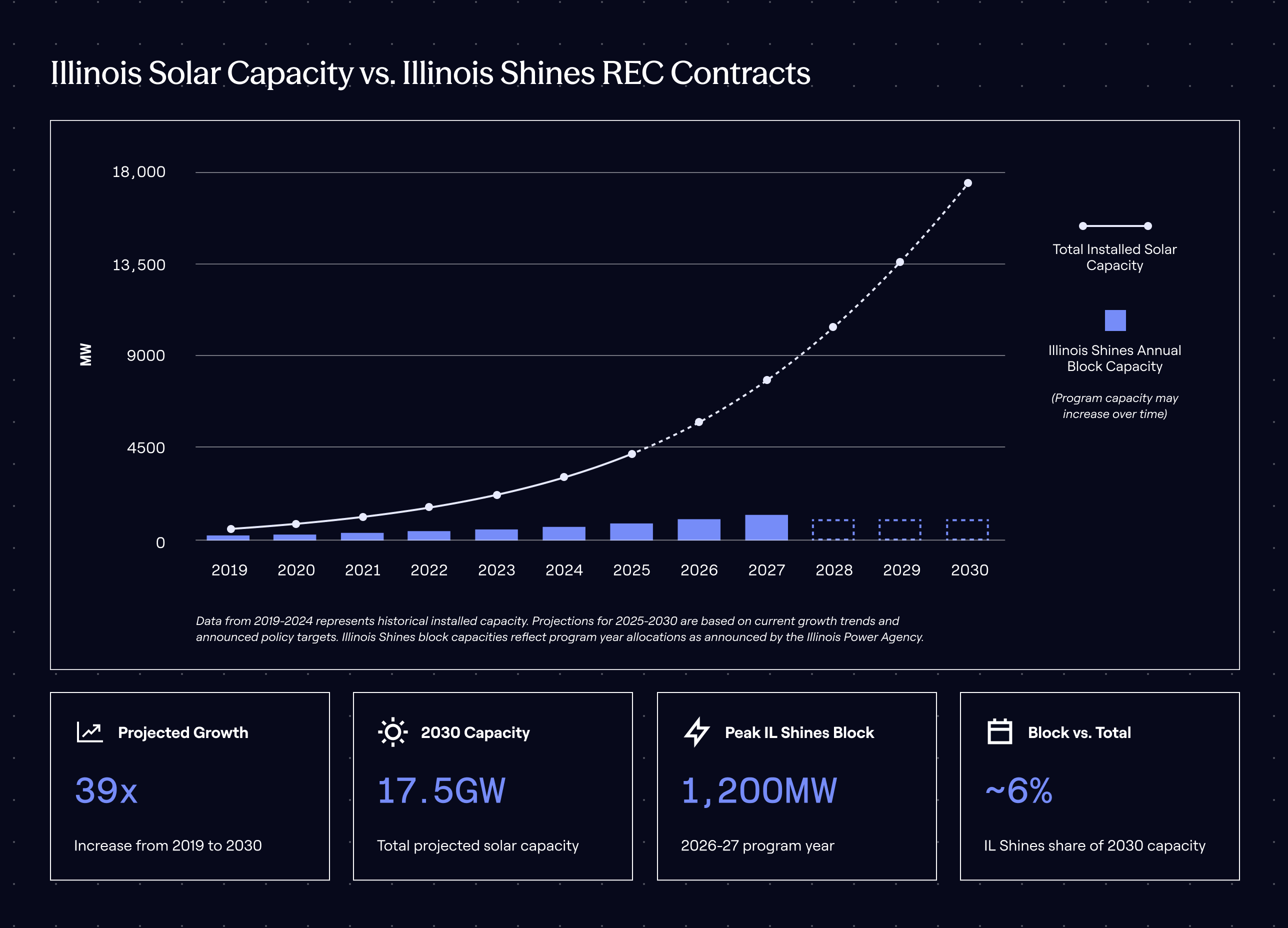

In 2016, there was just 55MW of installed solar capacity in Illinois. Today, over 6.6GW of solar energy powers the Prairie State. The state drove this rapid deployment by building a central policy framework that anchored the clean energy market around state-administered renewable energy credit (REC) contracts. These RECs, created by the Future Energy Jobs Act in 2016, sparked developer demand by offering 15-20-year state-backed contracts with revenue certainty comparable to a power contract.

10 years after FEJA, Illinois remains a hot market, with solar capacity expected to grow more than 1,700% by 2030, but the policy levers that drove its initial popularity are no longer the primary drivers of development decisions. As Illinois enters its next phase of growth, success is increasingly determined by factors that sit beyond the original policy design. Developers must evaluate how projects pencil without RECs, contend with greater scrutiny at the local level, and compete to serve AI-driven load growth.

In this piece, we examine these structural shifts shaping the solar market in Illinois: the uneven availability of RECs, the rise of local government as a development constraint, and the surge in localized power demand from data centers.

RECs: from assumption to advantage

Since its launch as the Adjustable Block Program, Illinois Shines has been consistently oversubscribed, with applications for community solar and large C&I projects exceeding available REC capacity in nearly every program year. In 2019, the program received applications representing 1.8GW of community solar projects, more than 10 times what administrators had expected. This year, all available capacity in the Traditional Community Solar category for the 2025-2026 program year was allocated to waitlisted projects on the first day the applications opened.

This scarcity has changed how developers think about their participation in Illinois Shines. Long queue times, uncertainty around award timing, and the financial underwriting challenges created by those uncertainties have led developers to increasingly underwrite projects on a “no-REC” base case, treating Illinois Shines awards as a scenario with upside IRR rather than a prerequisite for moving forward.

“A few years ago, we assumed that every Illinois project we looked at would be participating in Illinois Shines. We’re now increasingly seeing portfolios that only value RECs as upside, if at all, and our customers underwrite those profiles differently.” – Brian Newton, Program Manager, Development & Transactions

This shift has been made possible by a combination of structural and market changes, including declining solar costs and the emergence of credible alternative revenue streams. Developers are underwriting projects around load adjacency, merchant exposure, or future optionality tied to storage and reliability value. Some are monetizing RECs through third-party PJM trading arrangements rather than waiting through extended program cycles. In effect, Illinois is developing a two-track market: one that remains REC-anchored, and another that is incentive-agnostic.

The county-level constraint

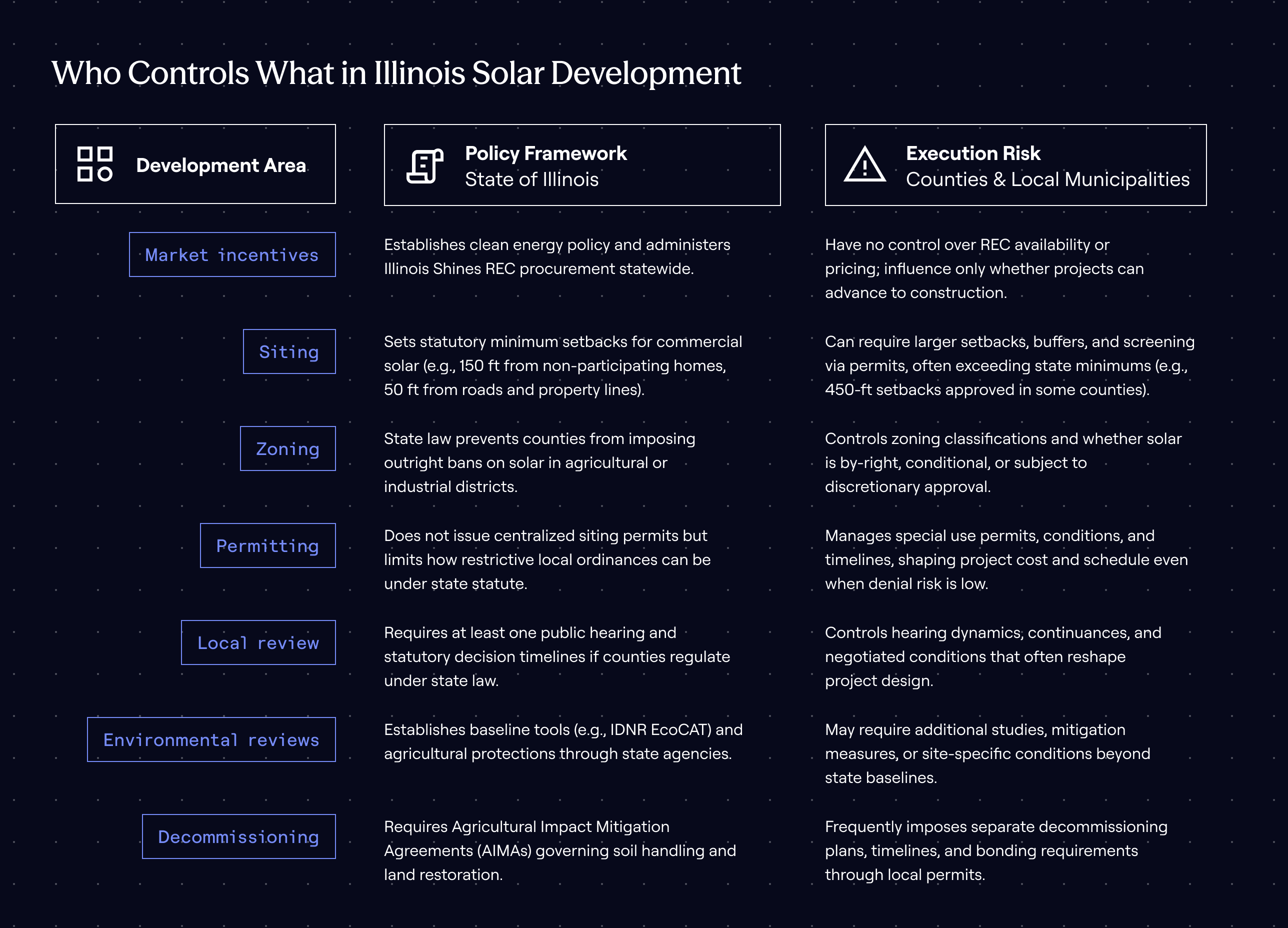

Strong statewide policy ignited solar development in Illinois, but the market’s next phase of growth will be shaped by decisions made at the local level. While state law limits a county’s ability to reject projects outright, local authorities retain significant control over how, when, and under what conditions projects move forward. Across nearly 100 solar projects totaling over 630 MW developed in Illinois, Euclid analysis shows that local approval and permitting processes have become a frequent and consequential source of development risk, transforming them from procedural steps into primary determinants of project timing, cost, and feasibility. Developers are adjusting their strategies to account for local risk earlier in development.

Counties exercise their influence most visibly through land-use approvals that allow them to impose project-specific conditions beyond statewide standards. Illinois law establishes minimum setback requirements, but counties can treat those standards as baselines rather than fixed limits, using discretionary zoning classifications and special use permits to require larger buffers on individual projects. Last fall, the Madison County Board approved a solar project only after the developer increased setbacks to 450 feet, nearly three times the state minimum. Conditions like these do not conflict with state law, but they affect site design, land-use efficiency, and development costs.

Financial assurance provides another point at which local authority reshapes project risk and capital timing. At the state level, agricultural restoration and post-project land recovery are governed by Agricultural Impact Mitigation Agreements (AIMAs) administered by the Illinois Department of Agriculture, which require developers to post decommissioning financial assurance equal to 10 percent of estimated costs on or before commercial operation, with additional security posted over time. Counties frequently accelerate that timeline. In Vermilion County, developers have been required to provide decommissioning financial assurance as part of the building permit process, and in November, the county approved multiple projects only after a developer agreed to post 100 percent of estimated decommissioning costs as a condition of receiving a building permit. These timing changes do not change the substance of decommissioning obligations, but they shift financial exposure earlier in development by increasing upfront capital requirements.

Similar dynamics appear in drainage and engineering review, where authority is divided across multiple local entities and standards are not fully aligned. Counties and county engineers often require detailed drain tile mapping, field investigations, and stamped drainage plans before issuing permits, even after zoning approval is secured. Drainage districts, which operate as independent units of local government, may separately require approval for modifications to district-controlled infrastructure. Developers must also reconcile local AHJ requirements with utility design standards that are often misaligned, increasing the likelihood of late-stage redesign and permit delays.

The result is a set of overlapping obligations that developers must reconcile during local review. It is increasingly common for projects to face two different decommissioning timelines, two cost assumptions, and two enforcement authorities – one tied to the state AIMA and another embedded in local permit conditions. While legally permissible, this dual-track framework has become a recurring friction point in hearings and negotiations, adding uncertainty to project budgets and schedules even when statewide policy remains supportive.

In response, developers are engaging earlier with the specific local processes that shape project viability. Drainage and soil specialists are being retained before site layouts are finalized, and coordination with county engineers and drainage districts often begins well ahead of formal permit submissions. Public outreach is starting earlier in the zoning process, and project designs are increasingly structured around conservative assumptions, including larger setbacks, additional screening, and layout flexibility, rather than optimized solely for production. County records show projects advancing through multiple redesigns, extended review cycles, and negotiated permit conditions that function as an additional development gate alongside interconnection and incentive timelines.

Demand changes everything

Rapid load growth, driven primarily by data center development, is increasingly shaping where and how solar projects pencil in Illinois. Northern Illinois, particularly the Chicago metropolitan area, has emerged as one of the most important data center hubs in the country, rivaling Dallas and Northern Virginia. What began as a steady stream of large-load requests accelerated sharply in late 2024, as utilities and regional planners began receiving inquiries for hundreds of megawatts of new demand at a pace that outstripped prior planning assumptions. Illinois policy is already responding to these pressures. Recent legislation directs the state to procure roughly 3 GW of battery storage by 2030, sharpening the focus on flexibility and reliability as load growth accelerates.

The impact is most pronounced in ComEd territory, where Illinois sits within PJM. Data centers arrive in large, concentrated blocks of demand and ramp up load over several years, tightening system conditions and increasing the value of projects that can deliver power close to where it is consumed. This dynamic is already influencing market structure. In December, the Federal Energy Regulatory Commission (FERC) directed PJM to draft new rules governing the co-location of large loads, such as data centers, with generation assets, including new frameworks for temporary, firm, and non-firm capacity arrangements. While PJM works through the details, the directive itself is telling: data center growth is no longer just a forecasting challenge, but a structural issue reshaping how capacity, interconnection, and reliability are managed.

For developers, the takeaway is that load growth is creating micro-markets within Illinois. Projects near major demand centers increasingly benefit from faster commercialization, alternative offtake structures, and future optionality tied to reliability and capacity value. Those farther from load centers face greater exposure to local opposition, interconnection congestion, and incentive timing risk. The Illinois market is no longer defined solely by access to programs, but by how quickly projects can deliver to areas where demand is growing fastest.

Change creates opportunity

These evolutions in Illinois do not impact its position as one of the most attractive solar markets in the country, but they do require developers to approach the state with greater selectivity and a more rigorous process.

The most successful projects will be able to withstand – or bypass – incentive timing risk, navigate local process with discipline, and align with emerging demand centers. Developers who can adapt to this required evolution will continue to find worthwhile opportunities in one of the country’s most consequential clean energy markets. Additionally, projects that can incorporate energy storage or otherwise provide capacity and reliability value will be particularly well-positioned as Illinois pursues its storage procurement goals and grapples with AI‑driven load growth.

Enjoying this deep dive?

Stay up to date on market insights for teams who build, buy, and finance renewable projects.