In 2023, PJM approved the Maryland Piedmont Reliability Project, a high-voltage transmission line intended to address growing reliability needs across the Mid-Atlantic as regional electricity demand accelerates. PJM forecasts that peak demand across its footprint will increase by roughly 70 GW over the next fifteen years, driven by a combination of data center growth, electrification, and broader load expansion. The 70-mile line runs entirely within Maryland, crossing Baltimore and Carroll Counties before ending in Frederick County.

While much of the incremental load growth is occurring outside Maryland, particularly in Northern Virginia, the consequences are regional. A more constrained PJM system increases the value of reliable, in-state generation for load-importing states like Maryland, which relies on regional markets for a significant share of its electricity. At the same time, Maryland is entering the most ambitious phase of its Renewable Portfolio Standard (RPS), first enacted in 2004, which requires that 50 percent of electricity sold in the state come from renewable resources by 2030. Within that mandate, solar carve-outs escalate rapidly, requiring utilities to source at least 14.5 percent of retail sales from solar by 2028.

This combination of rising regional system stress and accelerating in-state compliance obligations has widened the gap between Maryland’s statutory targets and the pace of deployable supply. The resulting challenge is not a lack of demand or policy ambition, but how to deliver new generation within the state’s land, siting, and permitting constraints. This deep dive explores how that gap increasingly channels development toward small-scale and community solar projects that can be built quickly, close to load, and within Maryland’s existing land-use governance.

Snapshot: Maryland policy framework

The following snapshot outlines the core policies, programs, and institutions that shape solar development in Maryland. These elements define how demand is created, how compliance is enforced, and why small-scale and community solar have emerged as the state’s primary source of solar power.

- Renewable Portfolio Standard (RPS): Requires 50% of electricity sold in Maryland to come from renewable sources by 2030, with a rapidly escalating solar carve-out reaching 14.5% by 2028.

- Community Solar Energy Generating Systems (CSEGS): Maryland’s permanent community solar program and primary pathway for small-scale deployment.

- Certificate of Public Convenience and Necessity (CPCN): A state-level approval issued by the Maryland Public Service Commission for certain larger energy projects.

- Maryland Public Service Commission (PSC): Administers CPCN approvals, SREC certification, and CSEGS compliance, making it the central authority governing project eligibility and execution.

- Key legislation:

- Brighter Tomorrow Act (2024): Introduces a 150% SREC compliance multiplier for eligible sub-5 MW, in-state projects, increasing SREC volume rather than price and aligning incentives with low-conflict siting.

- Renewable Energy Certainty Act (2025): Standardizes statewide solar siting rules and limits county veto power, shifting small projects toward administrative approval while preserving local design review.

The structural advantage for distributed solar

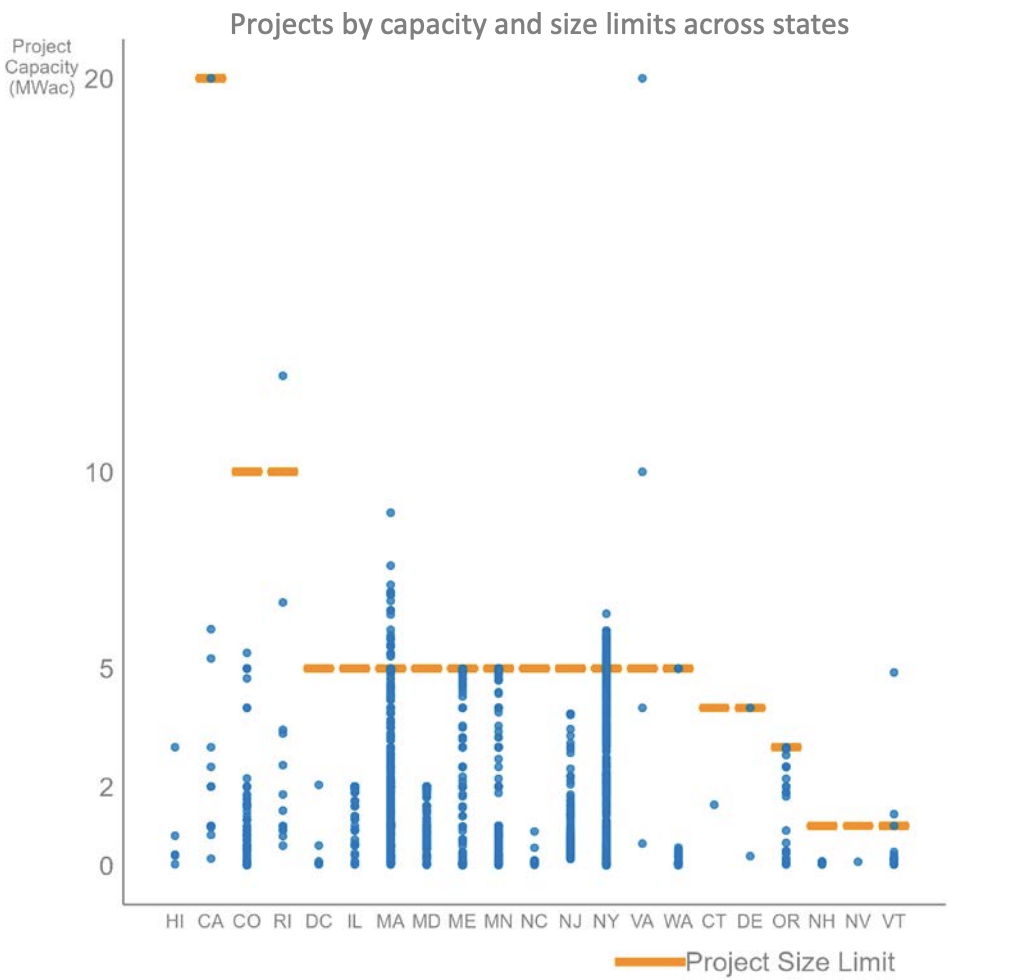

Analysis by the Maryland Solar Incentives Task Force defines the physical scale problem facing Maryland’s RPS: meeting the solar carve-out will require either more than 113 million square feet of rooftop solar or approximately 12,200 acres of land, including over 7,300 acres of farmland. Maryland is one of the most densely populated states in the country, with a state policy framework and local land use dynamics that intentionally slow the pace of large-scale development. As projects scale in size, developers face non-linear increases in execution risk driven by site assembly challenges, discretionary zoning approvals, CPCN requirements, and heightened exposure to appeals and litigation.

These dynamics materialize at specific size thresholds, most notably at 2MW, where projects trigger state-level review through the Certificate of Public Convenience and Necessity (CPCN) process administered by the Maryland Public Service Commission. For developers, the CPCN represents a step-change in execution risk:

- Expanded regulatory scope, including 20–30 additional requirements related to visual screening (e.g., “living fences” with native vegetation), environmental and conservation considerations, and community impacts.

- Higher upfront costs, including a non-refundable deposit equal to 1% of total project cost at filing. For a $15 million project, this requires a $150,000 cash outlay before construction risk is resolved.

- Extended timelines and appeal risk, as CPCN approvals are subject to challenge by local jurisdictions and other intervenors.

In this environment, large greenfield projects are difficult to build on a predictable timeline. Maryland’s incentive framework prioritizes projects that avoid these regulatory cliffs, rewarding smaller solar projects sited on rooftops, parking canopies, brownfields, landfills, and other previously disturbed parcels that can be entitled and built with greater certainty.

Maryland’s policy framework channels solar deployment toward small-scale projects by pairing capped, volume-based Solar Renewable Energy Credit (SREC) incentives and reduced execution risk under the Brighter Tomorrow Act (BTA) with separate low- to moderate-income (LMI) adders available to community solar, allowing these projects to achieve bankable returns despite land-use constraints and Alternative Compliance Payment (ACP)-capped pricing. In 2024, Maryland recorded the highest level of ACP payments in the program’s history, reflecting utilities’ inability to procure enough SRECs to satisfy the escalating solar carve-out. The Brighter Tomorrow Act (BTA) was enacted in 2024 in direct response to this growing gap.

The BTA materially affects the economics of small-scale solar by introducing a 150% SREC compliance multiplier for eligible sub-5-MW projects. By using certified SRECs, the policy increases the effective number of SRECs credited per megawatt-hour. Eligibility is intentionally aligned with Maryland’s land-use and permitting realities, prioritizing projects sited on rooftops, parking canopies, brownfields, and landfills. The eligibility structure limits the 150% SREC multiplier to community solar projects up to 2 MW when configured through aggregate net metering, while allowing projects up to 5 MW when sited on rooftops, parking canopies, or brownfields.

For a 2 MWdc community solar project, assuming a ~15% capacity factor and long-term SREC values of $60–70 per credit, the 150% SREC compliance multiplier can increase effective annual SREC output by approximately 1,300 credits, translating to roughly $80–90k of incremental, policy-backed revenue per year. Because the multiplier increases compliance value per MWh rather than relying on market pricing, it delivers predictable, high-margin revenue that improves IRR through earlier and more certain cash flows.

“When we’re supporting diligence on Maryland sites, the first screen is almost always size. Once a project crosses the 2MW threshold, the risk profile changes materially. You move from a permitting exercise into a quasi-judicial CPCN process with higher upfront costs, longer timelines, and real exposure to appeal. For developers, reviewing the system size isn’t about optimization at the margin; it’s about controlling execution risk and preserving schedule certainty.” — Kimberly Kuhn, Project Manager, Euclid Power

Beyond the SREC multiplier, the Brighter Tomorrow Act reduces operating and execution risk. It expands property tax exemptions and extends community solar tax eligibility through 2030. The Act also lengthens REC lifetimes to five years, standardizes permitting, and reinforces net metering frameworks. These changes support subscription-based revenue and remain compatible with existing LMI programs.

Stacking value with community solar

Maryland’s policy framework offsets community solar’s operational complexity with capital support and predictable revenue. The CSEGS program mandates that 40% of project output be reserved for low- and moderate-income subscribers. This boosts customer acquisition, verification, and servicing costs, which can pressure early cash flows and limit debt capacity. Maryland addresses these costs with layered incentives. These include volume-based SREC multipliers, LMI-specific adders, property tax relief, and stable retail subscription revenue. The compensation aligns with execution complexity, making risk-adjusted returns attractive for capable developers. This LMI support level matches national trends. By 2026, LMI capacity is projected to represent nearly 18% of U.S. community solar.

LMI support is structured through two graduated Areas of Interest (AOIs) that scale capital support with affordability and siting constraints.

- AOI 1 targets projects with moderate LMI participation and defined bill savings, offering direct grants of up to $2,000/kW-dc and income-verification reimbursement to offset higher servicing costs without materially impairing revenue.

- AOI 2 targets projects with deeper affordability commitments and constrained sites. These projects must supply 50% of output free to low-income households, with the rest delivered at a 25% discount. Eligibility is limited to landfills, rubble fills, and brownfields. Incentives for AOI 2 offset higher interconnection, site preparation, and execution costs found at these locations.

A recent $17 million funding announcement for community solar reinforces the state’s siting priorities, with about $12 million reserved for projects on landfills and brownfields. These projects must be fully subscribed by low-income households and deliver half their output at no cost. The remainder must be provided at a 25% discount. Projects on unconstrained sites have lighter affordability requirements but get less capital support. This approach shows how Maryland uses targeted support to guide development toward previously disturbed land.

At the project level, this translates into a clear and financeable cost profile. For a 2 MWdc community solar project, developers typically assume upfront subscriber acquisition costs of approximately $100 per kW-dc, or ~$200k, reflecting the 40% LMI requirement and the associated outreach and verification effort. Ongoing subscriber management, billing, and churn are modeled at ~$35k per year, consistent with NREL benchmarks, with income-verification costs partially offset by up to $10,500 in MEA reimbursement.

These costs are finite and controllable, unlike land-use, CPCN, and litigation risks seen with larger greenfield projects. In return, developers get a revenue stack that is hard to match elsewhere in PJM. Revenues come from policy-backed SREC uplift under the BTA, proven subscription demand, and LMI adders, all of which improve early cash flows. Maryland community solar lets experienced operators exchange operational complexity for faster deployment, lower regulatory risk, and more reliable returns in a dense, land-constrained, ACP-capped market.

Worth the (execution) risk

In Maryland, execution risk is driven by the interaction of project size, state approvals, and highly localized land-use governance. As projects scale, multiple regulatory thresholds converge, increasing exposure to cost overruns, schedule slippage, and litigation. Large greenfield projects are more likely to trigger CPCN review, require discretionary zoning approvals, and attract organized local opposition. By contrast, smaller projects sited on rooftops, parking canopies, brownfields, landfills, and other previously disturbed parcels typically face fewer discretionary hurdles and can proceed through administrative or by-right processes.

Developers who succeed in Maryland actively manage these thresholds through deliberate sizing, siting, and jurisdictional strategy. This is reflected in community solar projects clustering around 2 MW, even though eligibility extends up to 5 MW. In 2025, the passage of the Renewable Energy Certainty Act (RECA) reduced binary siting risk by shifting the state away from a fragmented, county-by-county regime toward standardized, statewide siting and design criteria. The law limits counties’ ability to impose more restrictive zoning or outright bans and moves approval of sub-5-MW projects toward administrative review under state standards. Counties have responded by aligning local ordinances with the new framework, as illustrated by Baltimore County’s adoption of state-consistent setback and zoning rules.

While RECA curtails local veto power, counties still control how they apply state standards. They do this through existing land-use processes, including special-use or conditional approvals. For example, in Caroline County, a 2 MW solar project was approved by the Board of Zoning Appeals with local design and siting conditions attached. This marks a shift from discretionary approval risk to administrative implementation risk, meaning developers may face delays or new requirements imposed during the permitting process rather than outright project denial. Developers still face local reviews that affect timelines and design requirements. However, local review no longer serves as a binary threat to compliant, small-scale projects.

The structure of Maryland’s permanent community solar program reinforces execution discipline. Once an application is complete, projects have 24 months to reach commercial operation. If they miss this milestone, projects must post additional security of $50 per kW to keep their queue spot. After 36 months, removal from the queue is possible. For a 2 MW project, missing deadlines could require a $100,000 security posting. This approach prices execution risk, discourages speculative development, and favors projects with predictable timelines.

Ongoing compliance focuses on administrative accuracy and operational readiness, not punishment. Certification, SREC eligibility, and program participation all depend on keeping system sizing, interconnection approvals, and reporting accurate. Formal decertification and civil penalties exist as backstops but are rarely used. The main consequence of non-compliance is a loss of eligibility, not fines or litigation. Developers must manage execution risk and administrative complexity to keep access to incentives and revenue. Those who face permitting delays or unresolved local issues suffer a downside, but it can be avoided.

The reward for the right developers

In this environment, with 2028 RPS deadlines looming, Maryland’s solar opportunity relies on projects which can move from entitlement to operation on predictable timelines. Small-scale and community solar — especially on brownfields, rooftops, and other low-conflict sites — fit this need. They avoid discretionary zoning, CPCN risk, and multi-year permitting.

Developers willing to manage subscriber complexity and LMI requirements can benefit from Maryland’s policy. The state’s framework turns operational effort into execution certainty and stable revenue. Instead of chasing scale in a tight market, Maryland rewards speed, careful site selection, and local delivery. In a tightening regional system, this makes community and distributed solar the most reliable way to add financeable generation.

Enjoying this deep dive?

Stay up to date on market insights for teams who build, buy, and finance renewable projects.